Blockchain for Beginners: Understanding the Basics Simplified

Published: 26 Jan 2025

Introduction

Imagine a world where every digital transaction you make is instantly recorded in a way that no one can tamper with. That’s the magic of Blockchain for Beginners. It’s a digital ledger system that securely stores data across a network of computers, making it transparent and nearly impossible to alter. But how does this work, and why does it matter to you? Let’s explore.

Blockchain is a technology that’s changing the way we think about digital data and transactions. Imagine a digital notebook where every page is a record, and once something is written, it can’t be erased or changed. That’s the basic idea behind blockchain. It’s like a secure, transparent, and permanent record-keeping system used by millions of people around the world.

In this post, we’re going to break down blockchain in simple, easy-to-understand terms. If you’re new to blockchain, don’t worry! We’ll explain the basics step-by-step so you can get a clear picture of how it works and why it matters.

Blockchain is more than just the technology behind cryptocurrencies like Bitcoin. It’s being used across industries like finance, healthcare, and supply chain management. In finance, it helps to make transactions safer and faster. In healthcare, it can keep medical records secure. And in supply chains, it helps businesses track products from start to finish, ensuring transparency and trust.

Understanding Blockchain for Beginners: The Basics You Need to Know

Definition: What is Blockchain?

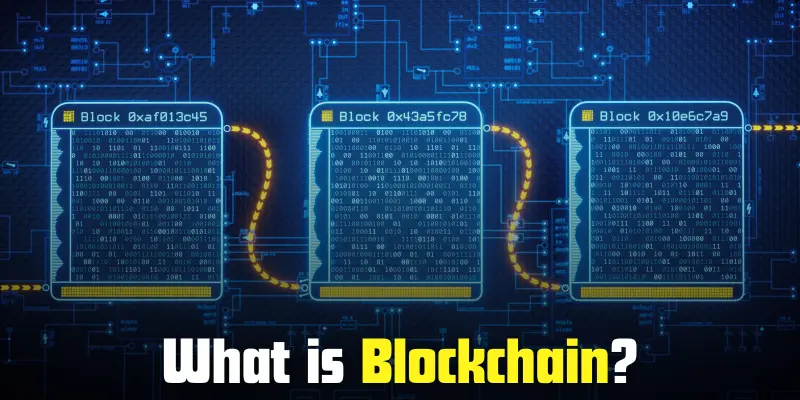

At its core, blockchain is a digital ledger or record-keeping system that stores information across a network of computers. Imagine it like a list of transactions that everyone can see but no one can alter once it’s added. Each piece of data is stored in a “block,” and these blocks are linked together in a chain (hence, “blockchain”). This technology makes it incredibly secure and transparent.

Why It Matters: The Revolutionary Power of Blockchain

Blockchain is revolutionizing how we store and share information. Traditionally, we rely on trusted middlemen like banks, government agencies, or companies to handle transactions. But with blockchain, there’s no need for a central authority. This decentralized nature allows people to trust each other without needing a third party. It’s faster, cheaper, and safer, making it an attractive option for a wide range of industries.

Analogy: Blockchain as a Public Ledger

Think of blockchain like a public notebook that everyone can write in but no one can erase from. Each time a new transaction or record is added, it’s written down in the notebook and can be viewed by anyone. However, once something is written, it’s permanent. You can’t change it or delete it, which makes it incredibly secure. The entire network of people using blockchain makes sure the information stays true and accurate.

How Does Blockchain for Beginners Work?

Blocks and Chains: How They Work Together

- A block is a collection of data (like transaction details) that is stored together.

- Chains link blocks in a sequence, where each block is connected to the previous one.

- Every block contains a unique code called a “hash,” which makes sure the data in that block is secure and cannot be altered.

- Once a block is added to the chain, it becomes permanent and cannot be changed, which makes blockchain so secure.

Decentralization: Why It’s So Important

- Blockchain doesn’t rely on a central authority (like a bank or government). Instead, it’s run by many computers (called nodes) across the world.

- This decentralized system makes it more secure because there’s no single point of failure. If one node goes down, the rest keep the system running smoothly.

- Since everyone on the network has a copy of the blockchain, it’s nearly impossible to tamper with the data without everyone noticing.

Nodes and Transactions: How Computers Work Together to Verify Transactions

- Nodes are computers in the blockchain network that store and validate the information (or transactions).

- Each time someone makes a transaction, it’s sent to multiple nodes for verification. This process ensures the transaction is legitimate.

- Nodes verify transactions by checking if the data matches and if the person has enough resources (like money or assets) to complete the transaction.

- Once the transaction is verified, it’s added to a new block, which is then linked to the chain. Everyone on the network updates their copy of the blockchain.

Key Benefits of Blockchain for Beginners

Security: How Blockchain Makes Transactions Safe and Secure

- Immutable Records: Once a transaction is recorded in a block, it cannot be changed or erased. This makes the data highly secure.

- Encryption: Blockchain uses advanced encryption methods to protect data, ensuring that only authorized users can access it.

- Decentralized System: Since blockchain doesn’t rely on a central authority, there’s no single point of failure, making it much harder for hackers to attack.

- Digital Signatures: Transactions are verified with unique digital signatures, which provide an extra layer of security and help prevent fraud.

Transparency: How Everyone Can See the Blockchain, But No One Can Alter It

- Public Ledger: Every participant in the blockchain network can view the entire blockchain, ensuring transparency and accountability.

- Permanent Records: Once data is added to the blockchain, it’s permanent and cannot be tampered with, so everyone can trust the information is correct.

- Open Access: Blockchain allows anyone to check the status of transactions, ensuring no hidden activities or secrets.

- Verification by All: Multiple parties verify each transaction before it’s added, making it almost impossible for fraudulent activity to go unnoticed.

Trust: How Blockchain Eliminates the Need for Middlemen

- No Third Parties: Blockchain allows peer-to-peer transactions without the need for banks, governments, or other intermediaries.

- Self-Validation: Transactions are verified by the network of nodes (computers), eliminating the need for a trusted third party to validate transactions.

- Built-in Trust: Because blockchain operates on a secure, decentralized network, users don’t need to rely on middlemen to ensure the legitimacy of transactions.

- Reduced Fraud: The transparency and immutability of blockchain records build trust among users, reducing the likelihood of fraud.

Efficiency: How Blockchain Can Speed Up Transactions and Lower Costs

- Faster Transactions: Blockchain transactions can occur in real-time or within minutes, compared to traditional systems that might take hours or days.

- Lower Transaction Fees: Since blockchain removes intermediaries like banks, it reduces or eliminates transaction fees, saving money for users.

- Global Accessibility: Blockchain allows for easy cross-border transactions without the delays or extra costs typically associated with international transfers.

- Automated Processes: Smart contracts on the blockchain can automate certain actions (like payments), further speeding up processes and reducing the need for human intervention.

Real-World Examples of Blockchain for Beginners

Cryptocurrency: How Bitcoin and Ethereum Use Blockchain

- Bitcoin: Bitcoin is the first and most well-known cryptocurrency that uses blockchain to enable secure, decentralized transactions without a middleman (like a bank).

- Ethereum: Ethereum is a blockchain platform that not only supports cryptocurrency (Ether) but also allows developers to build decentralized applications (dApps) using smart contracts.

- Secure Transactions: Blockchain ensures every Bitcoin or Ethereum transaction is recorded on the public ledger and can’t be tampered with, providing a transparent, secure way of transferring funds.

- Peer-to-Peer System: Both Bitcoin and Ethereum allow users to send and receive money directly to each other without needing an intermediary, thanks to blockchain technology.

Supply Chain: How Companies Like Walmart Use Blockchain for Tracking Goods

- Tracking Products: Walmart uses blockchain to track the journey of food products from the farm to the store, ensuring that each step is recorded and visible.

- Transparency: Blockchain allows all parties involved (suppliers, transporters, retailers) to access the same data, making it easy to verify the origin and status of products.

- Food Safety: If a product is contaminated or there’s a problem, Walmart can quickly trace it back to its source using blockchain, reducing the time it takes to remove unsafe goods from stores.

- Efficient Operations: By reducing paperwork and automating tracking, blockchain makes the entire supply chain process faster and more reliable.

Healthcare: How Blockchain is Used for Secure Patient Records

- Secure Health Data: Blockchain helps protect patient records by storing them in a secure, decentralized system, making it harder for hackers to access sensitive information.

- Control Over Data: Patients can control who has access to their health information, ensuring privacy and improving trust between patients and healthcare providers.

- Faster Access to Records: With blockchain, doctors and healthcare professionals can quickly and securely access a patient’s full medical history, improving treatment speed and accuracy.

- Reducing Fraud: Blockchain helps prevent the unauthorized use of medical records, ensuring that only authorized users can view or modify patient data.

Voting: How Blockchain Could Make Voting More Secure and Transparent

- Secure Voting Systems: Blockchain technology can be used to create tamper-proof digital voting systems, where every vote is recorded on a blockchain and cannot be changed or deleted.

- Transparency: Voters can verify their votes in real-time, ensuring transparency and preventing fraud or manipulation.

- Reduced Risk of Hacking: With blockchain, election data is decentralized, making it much harder for hackers to attack or alter voting results.

- Cost-Effective: Blockchain voting systems can be more cost-efficient than traditional methods, eliminating the need for paper ballots and physical polling stations.

Common Blockchain Terms for Beginners

Nodes: What Are They and How Do They Function?

- What is a Node?: A node is simply a computer that is part of the blockchain network. Every node keeps a copy of the blockchain and helps validate transactions.

- Role of Nodes: Nodes work together to verify and store transactions. They ensure the data is accurate before adding it to the blockchain.

- Distributed Network: Since there are many nodes across the world, the blockchain network is decentralized, meaning no single person or organization controls it.

- How Nodes Verify: When a new transaction occurs, nodes check it against the existing blockchain to confirm that everything is correct before adding it to the chain.

Cryptocurrency: What It Is and Its Relationship to Blockchain

- What is Cryptocurrency?: Cryptocurrency is a digital form of money, like Bitcoin or Ethereum, that uses cryptography to secure transactions and control new units.

- Blockchain’s Role: Blockchain is the technology that supports cryptocurrencies. It records and secures all cryptocurrency transactions in a public ledger.

- Decentralization: Unlike traditional money controlled by banks, cryptocurrencies are decentralized, meaning no single entity controls them. Blockchain ensures this system is secure and transparent.

- Example: When you send Bitcoin, blockchain records the transaction on the public ledger, ensuring that it’s safe, irreversible, and transparent.

Smart Contracts: A Simple Explanation and Their Benefits

- What Are Smart Contracts?: A smart contract is a self-executing contract with the terms of the agreement directly written into code.

- How They Work: Once the conditions of the contract are met (like payment or delivery), the contract automatically executes the terms—without needing a middleman.

- Benefits: Smart contracts are faster, cheaper, and more secure than traditional contracts because they’re executed automatically and can’t be altered.

- Example: If you buy a product using cryptocurrency, a smart contract could automatically release payment to the seller once the product is delivered.

Mining: What Does It Mean to Mine Blockchain Transactions?

- What is Mining?: Mining is the process of validating and adding new transactions to the blockchain. It’s done by powerful computers solving complex mathematical puzzles.

- Why Mining is Important: Mining ensures that the blockchain remains secure and that transactions are verified by the network.

- Proof of Work: Most blockchains, like Bitcoin, use a system called Proof of Work, where miners compete to solve puzzles and are rewarded with cryptocurrency for their efforts.

- Environmental Impact: Mining requires a lot of energy, which has raised concerns about its environmental impact. However, new systems like Proof of Stake aim to reduce energy usage.

Challenges of Blockchain for Beginners

Scalability: Issues Blockchain Faces with Handling Large Amounts of Data

- What is Scalability?: Scalability refers to a blockchain’s ability to handle a large number of transactions at once, without slowing down or becoming inefficient.

- Transaction Speed: As more people use blockchain, it can become slow. For example, Bitcoin’s blockchain can only handle around 7 transactions per second, while traditional systems like Visa can handle thousands.

- Network Congestion: When there are too many transactions at once, the blockchain can get crowded, leading to delays and higher transaction fees.

- Solutions: New blockchain technologies and upgrades, such as sharding and layer-2 solutions, are being developed to improve scalability and speed.

Energy Consumption: How Mining Consumes a Lot of Energy

- High Energy Demands: Blockchain mining, especially in networks like Bitcoin, requires huge amounts of electricity to power the computers that validate transactions.

- Proof of Work: The Proof of Work consensus mechanism used in Bitcoin mining requires miners to solve complex puzzles, which consumes a lot of computational power and energy.

- Environmental Impact: The high energy consumption of blockchain mining has raised concerns about its environmental impact, especially in regions where electricity is generated from non-renewable sources.

- Alternative Solutions: Some blockchains are moving to more energy-efficient methods, such as Proof of Stake, which require less computational work and energy.

Regulation: The Challenges of Regulating Blockchain Technologies

- Lack of Clear Laws: Blockchain operates in a decentralized manner, making it difficult for governments to regulate and control. There is a lack of clear legal frameworks around how blockchain should be used.

- Global Reach, Local Laws: Since blockchain is global, it’s hard for governments to enforce regulations. Different countries have different laws regarding cryptocurrencies and blockchain, creating confusion for businesses and users.

- Fraud and Security Risks: The anonymity of blockchain can lead to misuse, such as fraud or money laundering, making it difficult for regulators to track bad actors.

- Need for Balance: Regulators are working on finding the right balance between encouraging innovation and ensuring that blockchain is used in a safe and legal way.

Conclusion

So guys, in this article, we’ve covered Blockchain for Beginners in detail. Whether you’re looking to invest in cryptocurrency or simply curious about how blockchain is changing the world, understanding the basics is the first step.

My personal recommendation is to keep researching and stay up to date with new developments—blockchain is evolving fast! If you found this guide helpful, be sure to share it with others and subscribe for more beginner-friendly content. Let’s continue this learning journey together!

Frequently Asked Questions About Blockchain for Beginners

Blockchain is a digital ledger technology that records transactions in a secure, transparent, and unchangeable way. Each transaction is stored in a “block,” and these blocks are linked together to form a “chain.” It’s decentralized, meaning no single party controls it, and it’s used for things like cryptocurrencies, supply chains, and more.

Blockchain works by storing data in blocks, which are connected in a chain. When someone makes a transaction, it’s sent to many computers (nodes) that verify the information before it’s added to the chain. Once a block is added, it’s permanent and can’t be altered.

Cryptocurrency is digital money, like Bitcoin or Ethereum, that uses blockchain technology for secure transactions. It operates without the need for banks or governments, and transactions are verified by a network of computers rather than a central authority. Cryptocurrencies are decentralized and stored in digital wallets.

Smart contracts are self-executing agreements with the terms written directly into code. When the conditions of the contract are met, the contract automatically executes without the need for a middleman. They’re faster, cheaper, and more secure than traditional contracts.

Blockchain is secure because once data is added to the blockchain, it cannot be changed or erased. Each block has a unique code (hash) and is linked to the previous block, making it extremely difficult for anyone to tamper with the data. Additionally, the decentralized nature of blockchain means there’s no central point of control.

Yes! Blockchain has many uses beyond cryptocurrency. It’s used in industries like supply chain management (tracking products), healthcare (securing medical records), and even voting (securing election results). It’s a versatile technology that can improve transparency and security in many fields.

Nodes are individual computers connected to a blockchain network. They store a copy of the blockchain and help verify transactions before adding them to the chain. Nodes work together to ensure the integrity of the blockchain by confirming that all transactions are accurate.

Mining is the process of validating transactions and adding them to the blockchain. Miners use powerful computers to solve complex puzzles, and once they succeed, the transaction is added to the chain. In return for their work, miners are rewarded with cryptocurrency.

Got questions or thoughts on blockchain? Drop them in the comments below – we’d love to hear from you!

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

Leave a Reply Cancel reply